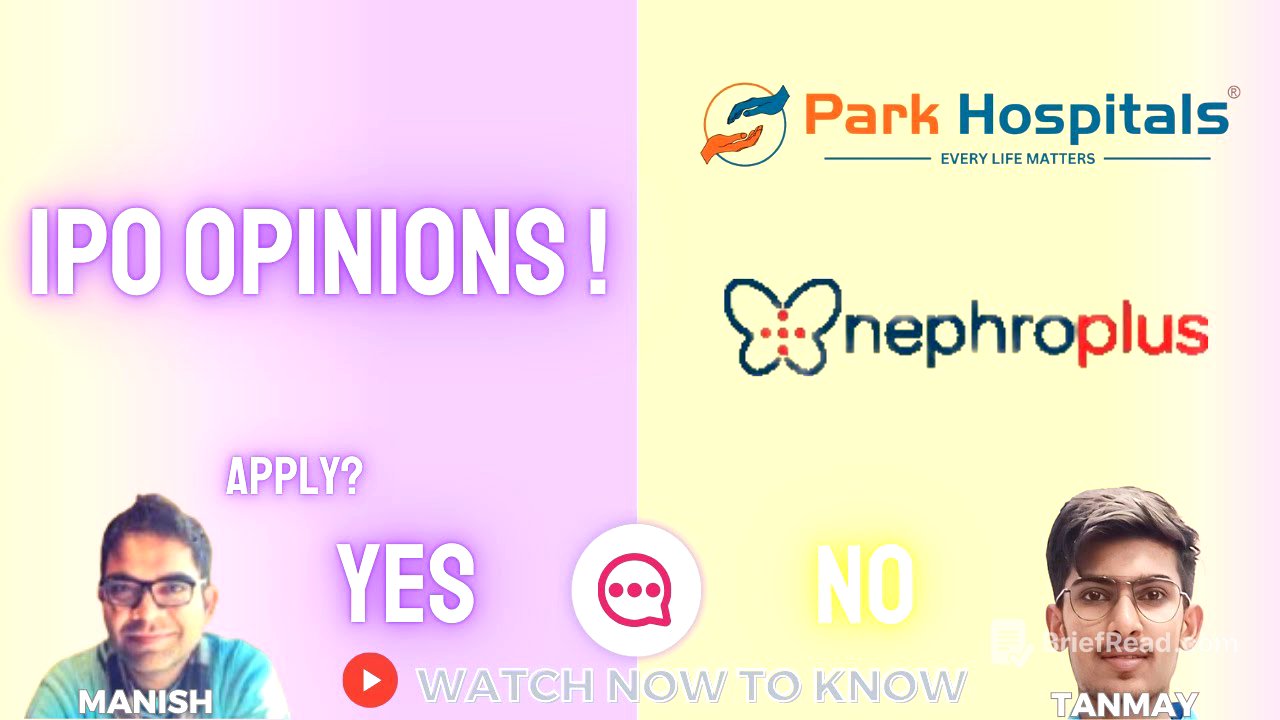

TLDR;

This video by Sunday Investing discusses two IPOs: Park Medi World and Nephrocare Health Services. The speakers provide an overview of each company's business model, financials, and potential investment considerations. They talk about Park Medi's focus on affordable healthcare and government schemes, and Nephrocare's position as a leading dialysis chain with international presence. They give their opinion on whether to apply for these IPOs or not based on their analysis.

- Park Medi World: Good company, good promoters, but skip due to valuation and dependence on government schemes.

- Nephrocare Health Services: Very interesting, good asset, attractive valuations, and high entry barriers. Likely to take a punt on this.

Opening Remarks [0:00]

The video is about the IPOs of Park Medi World and Nephrocare Health Services. The speakers clarify that they are not registered research analysts and their opinions are not qualified recommendations. They encourage viewers to do their own due diligence before investing. They also promote their YouTube channel for more such content.

Park Medi World (Mainboard) [2:00]

Park Medi World, incorporated in 2011, is a private hospital chain primarily operating in North India with a capacity of 3,000 beds as of March 2025. They operate 14 multi-specialty hospitals under the Park brand. The IPO consists of a fresh issue of ₹770 crores and an offer for sale of ₹150 crores, totaling ₹920 crores. The funds from the fresh issue will be used to reduce debt (₹380 crores), for capex of a new hospital (₹60.5 crores), purchasing new medical equipments (₹27.5 crores) and for unidentified acquisitions (₹302 crores).

Park Medi is the second largest private hospital chain in North India and the largest in Haryana, with 1600 beds in Haryana. They own 14 hospitals, with 8 in Haryana, 3 in Punjab, 2 in Rajasthan, and 1 in Delhi. The company focuses on acquiring hospitals. 55% of the revenue comes from acquired hospitals. They plan to build six more hospitals. The average revenue per occupied bed (ARPOB) is ₹26,500 to ₹27,000, indicating they operate in the affordable segment. Occupancy is at 64-65% in FY25 and 68% in H1, which is above industry average. A key point is that 84% of the revenue comes from government schemes like CGHS and state-run insurance companies, with a payment cycle of around 4.5 months, stretching the working capital cycle.

In FY23, the company had a top line of ₹1255 crores, EBITDA of ₹390 crores, and PAT of ₹228 crores, with a high EBITDA margin of 31.2%. However, FY23 H1 was affected by pent-up demand in hospitals, leading to higher margins. In FY24, revenue dropped by 2% to ₹1231 crores, EBITDA dropped to ₹310 crores, and PAT came to ₹152 crores due to new hospital acquisitions diluting margins. In FY25, the company grew by 13.2% with revenue of ₹1394 crores, EBITDA of ₹372 crores, and PAT of ₹213 crores. In H1, the company saw revenue growth of 17.1% to ₹807 crores, EBITDA of ₹217 crores, and PAT of ₹139 crores, with EBITDA margin constant at 26.9%. The market cap is ₹6,997 crores, with valuations at 18 and 12 times EV/EBITDA and 32.4 P/E ratio on FY25, and 16.5 times EV/EBITDA and 25 P/E ratio on FY26. A percentage of trade receivables is kept into disallowed claims from the government.

The company operates in the value segment, focusing on volume and higher occupancy rates. Competition is limited, but the dependence on government schemes (83% from CGHS) is a significant risk, with 11% of receivables in disallowed claims. The operations are not smooth. The closest competitor is Sarvodaya Healthcare. The company may always be valued cheaply compared to industry peers. The growth for FY26 is expected to be around 16-18%. The bed capacity is expanding from 3250 to 4900 in the next 3 years. The return ratios are expected to be around 16-19%. The company is fairly priced, but the speaker would skip the IPO.

The company is not factoring in anything for 26 or 27, it should be somewhere around 7 to 7 and a half%. Still the growth comes to around 15 to 20% even after factoring this margin should slightly improve like somewhere around half to you know percent and revenue should grow by somewhat around 700% which is said by management on television. The management wants to keep themselves in that affordable region affordable segment. There are no players at this listed space in the affordable segment in the organized segment in India. Competition is single hospitals and the government hospitals and not the private hospitals segment.

Sarvodaya is trading at around 22 to 23 times for the FI26 P ratio, while Park Medi is coming at 16 and a half times. Sarvodaya is technically trading cheaper than Park Medi if we just look at 27 numbers and based on the qualitative factors.

Nephrocare Health Services (Mainboard) [19:00]

Nephrocare Health Services, incorporated in 2010, provides end-to-end dialysis care through a network of clinics across India and select international markets. In India, they have 19 clinics across 288 cities in 21 states and 4 union territories. The IPO is ₹871 crores, with ₹350 crores fresh issue and the rest is offer for sale. The market cap is ₹4,600 crores, with approximately 18% dilution.

Nephrocare is the largest chain of dialysis care clinics in India and Asia, with over 520 clinics across four countries: India, Philippines, Uzbekistan, and Nepal. 60% of the revenue comes from India and 40% from overseas. In FY25, they treated 29,300 patients with 29 lakh treatments, holding a 10% market share of total dialysis patients in India. 80% of the dialysis market in India is unorganized, and Nephrocare has a 50% market share in the organized sector. The spend per dialysis treatment in India is $22, the lowest globally. In Saudi Arabia, where Nephrocare is entering, the realization per treatment is $220-$225, 10 times that of India, due to a highly regulated healthcare market.

It took Nephrocare 12 years to become EBITDA positive and they have been profitable for the last three to four financial years. 88 are green field, 259 are brownfield and 180 are PPP contracts. Standalone dialysis clinics are rare in India, except in Gujarat. The company partners with private and government hospitals. Outside of India, standalone clinics are more popular.

Out of the fresh issue, ₹136 crores is allocated towards debt reduction, ₹129 crores towards new dialysis centers, and ₹88 crores towards GCP. After this, the company should be almost debt-free. In FY23, the company had revenue of ₹437 crores, EBITDA of ₹49 crores, and a net loss of ₹12 crores. In FY24, they had a top line of ₹566 crores and good EBITDA margins of around 17-18%. In FY25, they had a top line of ₹756 crores, EBITDA of ₹166.6 crores, and PAT of ₹67 crores, with EBITDA margin around 22%. In H1, revenue was ₹473 crores and PAT was ₹14 crores, with an adjusted EBITDA margin around 24%.

For FY26, extrapolated numbers show a top line of ₹950 crores, EBITDA of ₹220 crores, and PAT of ₹120 crores. For FY27, expectations are around 20% top line growth, with ₹300 crores EBITDA and ₹200 crores PAT. On FY26, the valuation is at 17-18 times EV/EBITDA and 36 P/E, and on FY27, it is at 13-14 times EV/EBITDA and 23 P/E. The gray market premium is as good as zero. The anchor book was superb, with high-quality investors. The valuations are very juicy and attractive. There are no major receivable issues. The promoters are extremely great. The company is 4 and a half times larger than the second player.

The company is partnering with large private hospitals. The CFO is also good and the business is quite solid. There are very high entry barriers. An average dialysis chain in India takes almost 12 to 13 years to be EBITDA positive. The margins are fairly great and the growth is also quite reasonable. The speaker is likely to take a punt on this IPO.

Growth scenarios include signing PPP agreements, growing in the Philippines and Uzbekistan markets, entering KSA, and adjusted inflation revenue growth. Standalone dialysis centers in India are only viable in Gujarat. Overseas, the number of claims is significantly lesser but contributes to 40% of the revenue. The business is not easy to do and has come at a significant discount to Park. There is significantly higher competition in Park.

The speaker expects Nephrocare's PAT to be ₹67 crores in F25, ₹120 crores in FIR 26, and ₹200 CR7 in 27. The operational leverage is also very high. The anchor book included names like Polar Capital, Manual Life Global, Baroda BNP Paribas, Northeast Asset Management, and Fidelity SBI. Nephrocare Health is the world's fifth largest dialysis chain.

Closing Remarks [45:01]

The speakers covered Park Medi and Nephrocare, both healthcare-related companies. They will come back next week to talk about ICICI AMC and other companies in the pipeline. They thank everyone for joining and encourage viewers to join their YouTube channel.